Income from house property is a significant aspect of personal finance and taxation. Whether you own a property for self-use or generate rental income, understanding how to treat this income is crucial for accurate tax compliance. This guide provides an overview of the key considerations and guidelines related to income from house property and taxes. By grasping these fundamentals, you can effectively manage your house property income and optimise your tax obligations.

Types of income:

Income refers to the money or financial gain received by an individual, business, or entity over a specified period, typically measured on a monthly, quarterly, or annual basis.Income is a crucial aspect of personal finance and economic analysis. It plays a significant role in determining an individual’s or household’s standard of living. Here are some types of income :

- Salary Income:

Money earned from employment or work, usually paid in the form of a salary or wages. - Business Income:

Profit earned from operating a business or engaging in self-employment activities. - Rental Income:

Money received from leasing out properties or assets to tenants. - Investment Income:

Gains from investments like stocks, bonds, mutual funds, and real estate, including dividends, interest, and capital appreciation. - Dividend Income:

Money earned from owning shares in a company, usually distributed as a portion of the company’s profits to its shareholders. - Royalties:

Income earned by authors, musicians, artists, and inventors from the use of their intellectual property, such as books, music, art, or patents. - Pension and Retirement Income:

Regular payments received after retirement, typically from pension plans, annuities, or government-funded programs.

Calculation of GAV:

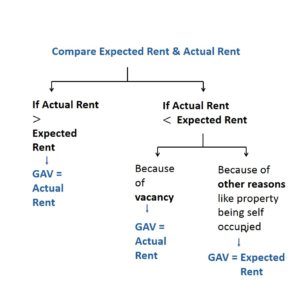

GAV stands for “Gross Annual Value.” It is a crucial factor in the computation of income from house property for tax purposes. The Gross Annual Value represents the notional or potential rent that a property can fetch during a financial year. The actual rent received, if any, may or may not be equal to the GAV. The calculation of GAV is different for self-occupied and let-out properties:

-

For Let-Out Property:

If the property is let out for the whole year, the GAV is the actual rent received during the year.

If the property is let out for part of the year, the GAV is the higher of the actual rent received or the potential rent for the remaining period of the year.

-

For Self-Occupied Property:

The GAV for self-occupied property is considered as zero. This means you don’t have to pay tax on the notional rental income if you live in the property.

Deductions Allowed:

The deductions allowed for income from house property are governed by the Income Tax Act, 1961. Here are the common deductions that can be claimed for income from house property:

-

Standard Deduction:

A standard deduction of 30% of the Net Annual Value (NAV) is allowed to cover various expenses related to repairs, maintenance, and collection of rent.

-

Interest on Home Loan:

For a self-occupied property, the interest paid on a home loan is eligible for a deduction of up to ₹2 lakh (₹1.5 lakh for loans taken before April 1, 2016) under Section 24(b) of the Income Tax Act. For let-out or deemed let-out properties, the actual interest paid can be claimed as a deduction without any limit.

-

Municipal Taxes:

The property tax paid to the local municipality is allowed as a deduction under Section 24(a) of the Income Tax Act.

-

Pre-Construction Interest:

If you have taken a home loan for a property under construction, the interest paid during the pre-construction period can be claimed as a deduction in five equal instalments from the year of completion of the construction.

-

Loss from House Property:

If the total deductions (including interest on home loan and municipal taxes) exceed the rental income, the resulting loss can be set off against other heads of income (like salary, business income, etc.) up to a maximum of ₹2 lakh.

Co-ownership and Multiple Properties:

-

Co-ownership Deduction:

When a property is co-owned by multiple individuals, each co-owner can claim deductions for interest on home loan and municipal taxes based on their respective ownership share in the property. This means that the total deductions (interest and municipal taxes) can be divided proportionately among the co-owners, and each co-owner can claim their share of the deduction in their income tax return.

Example, if a property is co-owned equally by two individuals, each can claim 50% of the interest on the home loan and 50% of the municipal taxes paid on the property.

-

Multiple Properties:

If you own more than one property, the tax treatment for income from house property varies based on whether the properties are self-occupied, let-out, or deemed to be let-out.

-

Self-occupied Properties:

Only one self-occupied property is considered for tax purposes, and its annual value is taken as nil. You can choose any one property as self-occupied, and the other properties are treated as deemed to be let-out.

-

Let-out Properties:

If you have let-out properties, the actual rent received from each property is considered as the Gross Annual Value (GAV). You can claim deductions for municipal taxes and the entire interest on home loan for each let-out property without any limit.

-

Deemed to be Let-out Properties:

If you have more than one property but don’t let out all of them, the remaining properties are treated as deemed to be let-out. For deemed let-out properties, the potential rent (fair rent) is considered as the GAV, even if the property is not actually rented out.

Self-Occupied vs. Let-Out Property:

Self-Occupied Property and Let-Out Property are two different categories of properties based on their usage, and they have different tax implications. Here’s a comparison between the two:

| Aspect | Self-Occupied Property | Let-Out Property |

| Definition | Property owned and used for the taxpayer’s residence. | Property rented out to others for rental income. |

| Tax Treatment | GAV considered as nil (No tax on notional rent). | GAV is the actual rent received or receivable. |

| Deductions Allowed | – Deduction up to ₹2 lakh on interest for home loan. | – Entire interest on home loan allowed as deduction. |

| – Deductions for municipal taxes allowed. | – Deductions for municipal taxes allowed. | |

| Number of Properties | Only one property can be treated as self-occupied. | Each let-out property is treated separately for tax. |

Handling Loss from House Property:

Handling loss from house property is an important aspect of tax planning, especially when you have more deductions (such as interest on home loan and municipal taxes) than rental income from the property. In such cases, you may incur a loss from house property. Here’s how you can handle the loss:

Set-off against Other Income:

The loss from house property can be set-off against income from other heads, such as salary, business income, or capital gains. The maximum allowable set-off is ₹2 lakh for a particular financial year. Any unadjusted loss after set-off can be carried forward to subsequent years.

Carry Forward Loss:

If the loss from house property cannot be fully set-off against other income due to the ₹2 lakh limit, the remaining loss can be carried forward for up to eight assessment years. It can be set-off against house property income in those future years.

Correct Filing of Tax Return:

Make sure to correctly file your tax return and report the loss from house property in the appropriate schedule or section as per the tax form used in your country.

Keep Records of Losses:

Maintain proper documentation and records of all expenses related to the property, such as interest on home loan, repair and maintenance expenses, and municipal taxes paid. This will help support your claim for the loss.

Taxation for Non-Residents:

Taxation for non-residents (NRIs) varies depending on the country in which they are earning income and their residency status in that country. In general, NRIs are subject to different tax rules compared to residents of the country. Let’s take a look at the taxation of NRIs from an Indian perspective:

Taxation of NRIs in India:

Residential Status:

In India, the residential status of an individual is determined based on the number of days they stay in India during a financial year. An individual is considered an NRI if they meet any of the following conditions:

- They stay in India for less than 182 days in the financial year.

- They stay in India for less than 60 days in the financial year and less than 365 days in the preceding four financial years.

Taxable Income:

NRIs are generally taxed on income earned or received in India. Income earned outside India is not taxable in India for NRIs.

Tax Deduction at Source (TDS):

Certain payments made to NRIs, such as interest, rent, or royalty, may be subject to TDS at higher rates than those applicable to residents.

Deductions and Exemptions:

NRIs are eligible for certain deductions and exemptions, similar to residents, based on the type of income earned. For example, deductions for home loan interest, insurance premiums, and investments may be available.

NRIs are required to file income tax returns in India if their total income in India exceeds the prescribed threshold or if they have any tax refund due.

In conclusion, understanding the intricacies of income from house property and its taxation is vital for effective financial planning. Properly treating house property income and complying with tax regulations can lead to optimised tax liabilities and enhanced financial stability. By adopting tax planning strategies, utilising allowable deductions, and staying updated with recent changes, individuals can navigate the complexities of taxation, maximise savings, and achieve their long-term financial goals.

Recent Comments