P2P (Peer-to-Peer) lending, also known as social lending or crowdlending, is an innovative financial model that connects borrowers directly with individual investors through online platforms. It allows borrowers to access loans without traditional financial intermediaries like banks, while investors can earn interest by funding these loans. P2P lending has gained popularity due to its simplified application process, faster approvals, and potential for higher returns compared to traditional savings accounts. However, it also comes with certain risks, and understanding its mechanics is crucial for both borrowers and investors

Understanding P2P Lending Process :

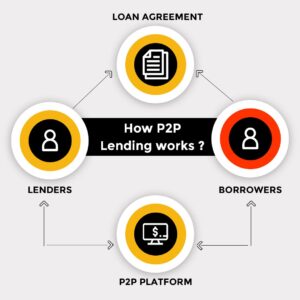

The P2P lending process involves several key steps. Borrowers begin by creating loan listings on the platform, detailing the loan amount, purpose, and interest rate. Investors review these listings and decide which loans to fund based on risk and return factors. Once a loan is fully funded, the borrower receives the loan amount, and regular repayments begin. The P2P platform facilitates loan servicing, handling collections, and distributing payments to investors. Throughout the process, the platform may conduct credit assessments to evaluate the creditworthiness of borrowers. Understanding this process is crucial for both borrowers and investors to participate confidently in P2P lending.

Pros and Cons of P2P Lending :

Evaluating the pros and cons of a particular subject helps in understanding the strengths and weaknesses, enabling individuals to make informed decisions and assess the overall impact of a choice or action. By considering both the pros and cons, individuals can weigh the benefits against the drawbacks to make well-rounded and balanced judgments.

Pros:

- Access to Finance: P2P lending offers borrowers an alternative funding source, especially for those with limited access to traditional loans.

- Competitive Rates: Borrowers may secure lower interest rates compared to traditional lending channels.

- Diversified Investment: Investors can diversify their portfolio by funding multiple loans, potentially increasing returns.

- Streamlined Process: The online platform provides a simplified and efficient loan application and approval process.

Cons:

- Default Risk: There is a risk of borrowers defaulting on their loans, leading to potential losses for investors.

- Limited Regulations: P2P lending may lack comprehensive regulatory oversight, exposing participants to certain risks.

- Lack of Liquidity: Investors may face challenges in selling their loan investments before the loan term ends.

- Credit Risk Assessment: Not all platforms may have robust credit assessment procedures, increasing investment risks.

Regulation and Legal Considerations :

P2P lending, being a rapidly growing industry in India, has attracted attention from regulatory authorities to ensure consumer protection, fair practices, and financial stability. The Reserve Bank of India (RBI) plays a pivotal role in overseeing and regulating P2P lending platforms in the country. In 2017, the RBI issued guidelines for P2P lending platforms to promote a safe and transparent ecosystem for borrowers and lenders.

Key Aspects of Regulation:

Registration and Eligibility: P2P lending platforms must be registered as non-banking financial companies (NBFC-P2P) with the RBI.

Limit on Exposure: To protect lenders from excessive risk, the RBI sets limits on the maximum amount a lender can lend to a single borrower across all P2P platforms.

Risk Assessment and Disclosure: P2P lending platforms are required to conduct a comprehensive credit assessment of borrowers, including creditworthiness checks.

Fair Practices and Transparency: The RBI mandates that P2P lending platforms must maintain fair practices, transparency, and standardisation in the operations of the platform.

Data Security and Privacy: P2P lending platforms must comply with data security and privacy regulations to protect the sensitive information of borrowers and lenders.

How to Get Started with P2P Lending:

Getting started with P2P lending is relatively simple and can be done in a few easy steps:

Research: Begin by researching various P2P lending platforms operating in India. Compare their offerings, interest rates, fees, and borrower profiles to find a platform that aligns with your investment goals.

Registration: Once you have chosen a platform, register as an investor by providing the necessary details and completing the verification process.

Fund your Account: Deposit the desired amount into your P2P lending account, which will be used for lending to borrowers.

Monitor and Reinvest: Keep track of your investments regularly. As you receive repayments and interest, consider reinvesting in new loans to compound your returns.

Understand Risks: Familiarise yourself with the risks associated with P2P lending, including the possibility of borrower defaults. Be prepared for both successful and unsuccessful loans.

By following these steps and conducting due diligence, you can confidently embark on your P2P lending journey and potentially reap attractive returns on your investments.

P2P Lending: A Win-Win Solution:

P2P lending presents a win-win solution for both borrowers and lenders, revolutionising the way individuals access funding and invest their money.

Accessibility: P2P lending offers an alternative source of funding to borrowers who may face challenges obtaining loans from traditional financial institutions.

Quick Processing: Borrowers experience faster loan processing times through online platforms, meeting their urgent financial needs.

Competitive Rates: P2P lending platforms often offer competitive interest rates, potentially lower than those of traditional lenders.

Attractive Returns: P2P lending provides investors with an opportunity to earn higher returns compared to traditional investment options like savings accounts and fixed deposits.

Diversification: Investors can diversify their investment portfolio across multiple borrowers, spreading risk and increasing the likelihood of steady returns.

Promoting Entrepreneurship: P2P lending encourages entrepreneurship by providing easier access to capital for small businesses and startups.

Economic Growth: Facilitating access to credit supports economic growth by stimulating consumption and investment activities.

P2P lending has revolutionised the lending landscape, offering borrowers and investors an alternative financial model. With its streamlined process and potential for competitive returns, P2P lending has attracted a growing user base. However, participants must be aware of the risks involved and make informed decisions.. As technology and regulations evolve, the future of P2P lending holds promising advancements, providing both borrowers and investors with viable options to meet their financial needs and goals.

Recent Comments